CPAB 2025 Interim Inspections: A Global Call for Consistency in Assurance

- Posted by admin

- On November 5, 2025

- 0 Comments

The Canadian Public Accountability Board (CPAB) released its 2025 Interim Inspections Results with findings that carry significance well beyond Canada. Of the 59 audit files inspected at the country’s four largest firms, 9 contained significant deficiencies. At other inspected firms, 4 out of 10 files were found deficient. The report reinforces recurring weaknesses in revenue audits, accounting estimates, and the valuation of financial instruments.

These are not isolated issues. They mirror concerns voiced by regulators across multiple jurisdictions, reflecting a shared set of challenges for the assurance profession worldwide.

Technology: Opportunity and Oversight

Auditors are increasingly relying on technology, including advanced data analytics and artificial intelligence. CPAB noted instances in which such tools were used without sufficient validation or professional skepticism, raising quality concerns. Quality management standards such as CSQM 1 in Canada and ISQM 1 globally require rigorous oversight, yet inspection findings suggest uneven implementation.

Regulators elsewhere have made similar observations. The PCAOB in the United States, the UK’s FRC, and European oversight bodies have all warned that technology, while transformative, can introduce risks if not subject to consistent and disciplined practices. The message is uniform: technology does not replace auditor judgment—it must reinforce it.

Group Audits: A Consistent Weak Link

The report also highlighted deficiencies in group audits, particularly in the supervision of component auditors and the evaluation of fraud risks across entities. With the revised CAS 600 now in effect, expectations around group auditor oversight are higher. CPAB’s findings show that firms are still adapting to these requirements.

This challenge is not uniquely Canadian. U.S. and European regulators continue to report shortcomings in cross-border group engagements. Oversight gaps, inconsistent application of accounting policies, and weak responses to fraud risk are recurring themes. Group audits remain one of the most complex areas of assurance, yet the weaknesses identified are strikingly consistent worldwide.

Technical Accounting Expertise: A Shared Gap

Another common concern is the lack of sufficient technical accounting expertise in complex areas such as revenue recognition, financial instruments, and fair value estimates. CPAB’s findings on valuation and estimates reflect a broader global trend. Regulators in the U.S., UK, and Europe have all stressed that the depth of technical knowledge within audit teams is uneven, leading to recurring deficiencies in judgment-heavy areas.

In capital markets that are increasingly interconnected, this gap has consequences beyond individual jurisdictions. Investors and regulators alike expect assurance teams to bring consistent, high-quality technical expertise, regardless of geography.

Assurance Is Global

Inspection results are reported at a national level, but the lessons are universal. Whether the regulator is CPAB, PCAOB, or the FRC, the themes are the same: technology must be governed by standards, group audits require robust and practical oversight, and complex accounting areas demand deep expertise.

Assurance cannot afford to remain siloed by jurisdiction. Capital flows are global, investor confidence is global, and therefore, audit quality must be global. The CPAB’s 2025 interim results are a reminder that the profession faces common challenges that demand common solutions.

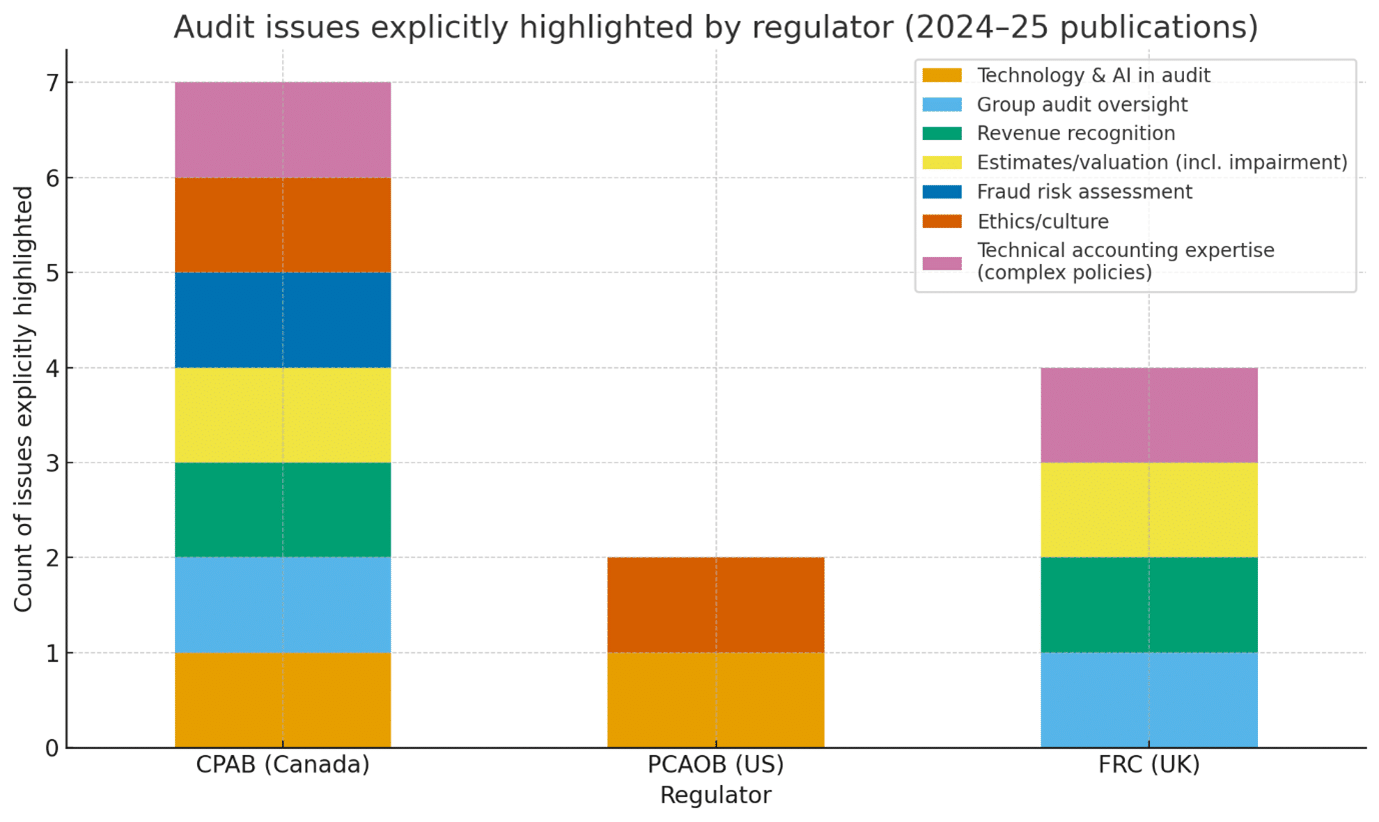

Comparative Visualization

Figure 1: Issues explicitly highlighted by regulators in 2024–25 publications

- CPAB (Canada): highlighted all major issues, including technology, group audits, revenue, estimates, fraud risk, ethics/culture, and technical expertise.

- PCAOB (US): in its 2025 inspection priorities, explicitly emphasized technology/AI and ethics/culture. Other areas are frequently noted in past reports but were not listed as 2025 priorities.

- FRC (UK): in its 2025 Annual Review of Audit Quality, highlighted group audit oversight, revenue recognition, impairment/estimates, and technical accounting expertise.

KNAV Comments

The CPAB’s 2025 interim results make one point abundantly clear: the challenges facing assurance professionals are not confined to any single jurisdiction. Whether in Canada, the United States, or the United Kingdom, regulators continue to identify deficiencies in technology use, group audit oversight, and technical accounting expertise.

While each regulator may emphasize different aspects—CPAB addressing fraud risk and ethics, PCAOB spotlighting technology and firm culture, and the FRC underlining group audit execution and impairment testing—the underlying message converges. Audit quality issues transcend borders.

To safeguard global capital markets, the profession must move toward consistent, practical standards that support high-quality assurance everywhere. Investors and stakeholders are not looking for national benchmarks—they expect reliability and comparability regardless of geography. Audit firms, regulators, and corporate leaders must recognize that assurance is global, and only through coordinated practices can confidence be strengthened across all markets.

0 Comments